Thailand Cambodia Overlapping Claims Area. Is a settlement in sight?

Reports that senior Thai and Cambodian ministers agreed to push forward with talks to develop the Thailand-Cambodia Overlapping Claims Area (‘OCA’), a disputed portion of the Gulf of Thailand, marks a potential thawing of a dispute which has festered for two decades and has prevented exploration for oil and gas in what many experts believe is a highly prospective area.

What is the Thailand Cambodia OCA?

The actual overlapping claims area is a 27,000 sq km section in the Gulf of Thailand that is claimed by both countries. Previous estimates have suggested the area potentially contains up to 11 trillion cubic feet of natural gas as well as large quantities of condensate and oil. The area is delineated in the west by Cambodia’s 1972 claim and in the east by Thailand’s 1973 counterclaim. The southern boundary is marked by the 1991 Cambodian-Vietnam maritime border.

Source: Arsana and Schofield

The Gulf of Thailand has well established oil and gas fields stretching the length of peninsular Thailand and into Malaysia, but the central and eastern portions of the gulf have never been properly explored due to the dispute.

Talks to overcome this have been largely stalled since the early 2000’s. A 2001 MOU between Thailand and Cambodia outlined an agreed framework to settle the maritime dispute, but flare ups in political tensions and issues over land border demarcations between the countries – particularly around the Preah Vihear temple – have meant that formal discussions never progressed beyond high level ‘talks about talks’ and the presentation of initial proposals by working groups. In 2009, in the midst of exacerbated tension between the two countries, the Thai Cabinet voted to scrap the 2001 MOU, adding further uncertainty as to how both countries would formally handle the dispute.

CLC Asia has covered these tensions in detail in our 2010 note on the subject (“The struggle over oil and gas resources“). Needless to say, many of the issues that led to these tensions could rear their ugly heads at an inopportune time, particularly if nationalist sentiment on both sides of the border were whipped up. But for the moment they remain calm, and we suspect that with the passage of time, tensions over these issues may have lowered somewhat for talks to at least commence.

What’s different this time?

Put simply, Thailand faces declining natural gas production and needs to shore up its energy security. Similarly, Cambodia is totally dependent on foreign sources of energy and has been unsuccessful in developing its own industry – after more than two decades of trying.

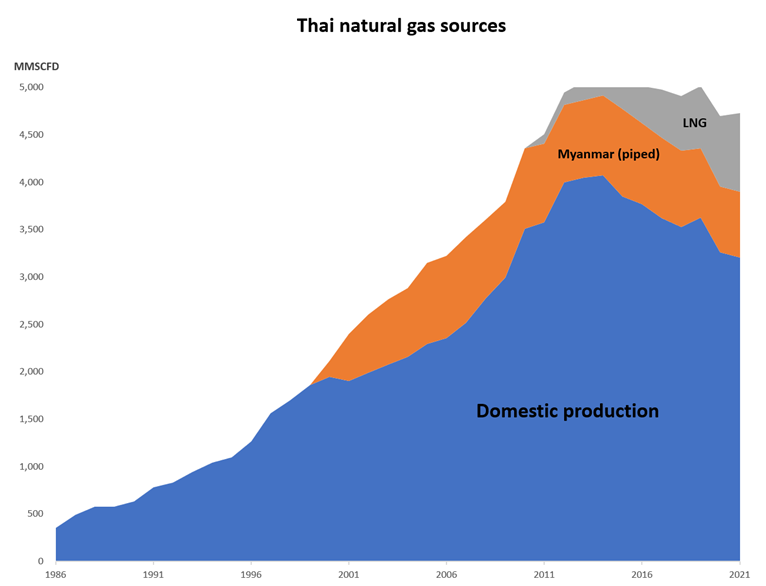

From a peak of 4073 MMSCFD of domestic natural gas production in 2014, Thai domestic production has been trending down, with 3204 MMSCFD being produced by the end of 2021, according to figures from the Thai Energy Policy Office. As domestic demand has increased, so has reliance on imports. From next to zero natural gas imports in 2000, Thailand imported 1512 MMSCFD of natural gas in 2021, with approximately half piped in from Myanmar.

But given the latter country’s ongoing instability, Thailand is increasingly reliant on expensive LNG imports, which have increased 8-fold since the first shipment in 2011. As Thailand’s own sources deplete, these imports will only increase. And while the government and PTTEP make the right noises about increasing domestic production, it is really a matter of delaying the inevitable as domestic sources dwindle.

Cambodia on the other hand is totally reliant on oil and gas imports, with expensive imported diesel fuel being a key foundation of its power generation. In the early 2000’s, the country fancied itself as a new oil and gas producer, but its efforts have been lacklustre. Potential partners, including Chevron and China National Offshore Oil Corporation (‘CNOOC’) both pulled out, with insiders citing frustration over the lack of certainty on taxation and licensing issues by Cambodian authorities.

Nevertheless, grand deadlines were set by the government, including an auspicious 12/12/12 date touted by the country’s leadership as the day Cambodia would produce its first barrel of oil. Unfortunately, the date came and went without a whimper, leaving plans to develop Cambodian Block A in tatters.

Singapore based Kris Energy then tried its hand at developing the block, only to walk away as well-known reservoir issues and wildly optimistic forecasts made production unfeasible.

A lot is at stake. From the Cambodian perspective, after two decades of no progress on their indigenous oil and gas production, they enter a third decade of the 21st century still totally reliant in energy imports.

Politically, from the Thai side, higher electricity bills and the potential for fuel shortages have been identified as sensitive issues according to sources who have worked closely with the Thai Ministry of Energy. One advisor to the Ministry of Energy described the Thai government of being ‘petrified’ of brownouts during Thailand’s hottest season in April.

Economically, Thailand’s massive petrochemical industry – the largest in ASEAN relies on feed from Gulf of Thailand sources, and falling domestic supplies have forced the industry to reconsider its mix of feedstock and downstream product, as well as looking for investment opportunities offshore, closer to more accessible feedstock.

So what are the solutions?

Revenue sharing

Exploration in the overlapping claims area has never been permitted. Industry experts expect that most of the exploitable reserves are located towards the Thai side of the OCA. The geological formations which contain most offshore oil and gas reserves in undisputed Thai waters extend into the OCA. But how to share revenues when no one is certain of what exactly lies beneath the seabed is a major complication.

Geologically, as was predicted by experts (and subsequently discovered by Kris Energy), the Cambodian side of the overlapping claims area is likely to face more challenging drilling and extraction issues, impacting feasibility.

Both countries have presented competing proposals over the years. The Cambodian proposal divides the disputed area in a checkerboard fashion, creating at least 14 different blocks. Revenues and management of the blocks would be shared equally on a 50/50 basis.

The main Thai counterproposal insists that the disputed area be divided into three parallel zones running north to south, with the revenue from the central zone to be shared equally on a 50/50 basis. The share from the outer zones would be weighted in favour of the country adjacent to that area. In the past, Thailand’s starting position was that weightings be 80/20 to Thailand on the western side of the OCA and 80/20 to Cambodia on the eastern side of the OCA.

Thailand wins big, regardless of the model

Even with a Cambodian proposal for 50/50 revenue splits, Thailand would be the largest beneficiary, primarily due to Thailand having a more sophisticated and developed oil and gas industry, which would be needed to both develop the blocks and then refine the product. There is next to no domestic capacity in Cambodia, and regardless of the revenue sharing model, Thai producers and contractors would need to undertake the bulk of the work in the overlapping claims area, and Thai companies would walk away the biggest winners.

What will bring both sides to finally settle this dispute?

In 2010, when CLC Asia first wrote about this issue, we posited three key factors which needed to be addressed before a resolution was possible in the Thailand Cambodia OCA. These were:

- Cambodia giving up territorial claims over the Thai island of Koh Kut;

- Development of a Cambodian oil and gas industry to better take advantage of opportunities from the OCA; and

- Increased Thai gas demand forcing Thailand to swallow its diplomatic pride and work with Cambodia.

We review them in light of the events of the past 13 years to see how they stack up.

A change of philosophy to maritime border demarcation

In our 2010 note, an expert we spoke to suggested a ‘good starting’ point for negotiations was for Cambodia to accept that its territorial claim over half of Koh Kut (an island ceded by France to Siam in 1904) does not have any legal basis. Cambodia could instead accept the median line principal to delimit the territorial sea and continental shelf between the two countries.

We recently touched base with the same expert, who stated that it is likely nothing has changed from that perspective, and that without this concession from Cambodia, it would be unlikely that meaningful progress could be made.

A more mature Cambodian oil and gas industry

Given the lack of any real incentive from the Thai side in 2010 to rush into talks, Cambodian advisors admitted to us that the only real way for Cambodia to strengthen its bargaining position against Thailand was to allow the domestic Cambodian oil and gas sector to mature, so that at some point in the future, their companies and contractors would be better placed to more fully capture the economic benefits from the development of fields in the overlapping claims area.

The thirteen years since have proven this was too much to hope for. Cambodia is still highly dependent on foreign fuel imports, and as its economy grows, it will be even more so. Though it was never expected that the domestic Cambodian sector would ever match Thailand’s 45-year old industry, failure to extract any oil and gas at all, due to a combination of technical, regulatory and administrative factors, means that they are still at square one.

Increased gas demand by Thailand

The thinking in 2010 was that Thai gas demand would continually increase. And while Thai gas consumption did indeed increase from 4,039 MMSCFD in 2010 to 4,764 MMSCFD in 2015, it has since leveled off and then decreased to 4,395 MMSCFD in 2021. However, maintaining this level of supply means that new sources have to be found, and with imports becoming increasingly expensive, Thailand has little choice but to start looking at the OCA as an option. It is clear that Thailand’s increasing need (but not yet desperation) to maintain energy security has forced it back to the negotiating table. And while Thailand’s current rulers may fancy themselves as being able to deal with the miliary junta in Myanmar to maintain piped gas supply, hedging their bets given the instability there is a wise move.

Joint Development Area the only solution

At the present time, a Joint Development Area (JDA) seems to be the only realistic solution to both countries to develop and manage the overlapping claims area in the Gulf of Thailand.

Politically, a JDA helps gloss over any political differences, allowing parties to ‘agree to disagree’ while moving ahead with the real work on exploration. Thailand already runs a successful JDA with Malaysia which despite competing territorial claims, has worked successfully for decades, and there is no reason why this model couldn’t be copied.

The real issue is whether we are just seeing more talks about talks or whether there finally is a chance that this is moving forward.

Thailand faces elections this year, where a change of government could make things unpredictable. Well established nationalist voices in Thailand would find even the appearance of ceding any sliver of sovereignty to the Cambodians unacceptable. If they do, there is a reasonable risk they could cause havoc either during any potential talks, or when a draft proposal comes before parliament for consideration.

One Thai official who is familiar with border disputes stated that the whole discussion is a non-starter unless Cambodia removes its claim on part of Koh Kut. Cambodian advisors we have spoken to simply hope that the topic of Preah Vihear doesn’t rear its head from the Thai side – a sure fire way to derail any talks.

Thai officials we have spoken to aren’t necessarily convinced the latest round of announcements from senior ministers will amount to much. One gave them no more than a 60% chance of the talks going anywhere.

This article was first published at www.clc-asia.com where it is available for download in PDF format.